HRA vs. HSA: Understanding The Difference

Health insurance provides financial protection to offset the medical costs associated with unexpected illness or injury. A health insurance policy allows enrollees to pay less for covered in-network health care, such as preventive care, vaccines, screenings, and check-ups than if they were uninsured.

A Health Savings Account (HSA) and a Health Reimbursement Arrangement (HRA) are two widespread tax-advantaged health benefits that can be used to complement a health insurance policy. Although an HSA and an HRA have some similarities, they differ in set up and accessibility.

What Is a Health Reimbursement Arrangement (HRA)?

A Health Reimbursement Arrangement (HRA) isn’t traditional health insurance. Instead, it is an employer-funded group health plan where an enrolled employee is reimbursed tax-free for qualified medical expenses up to a fixed dollar amount each year. Whether or not you’re eligible to enroll in an HRA is determined by your employer.

Since individual employers fund it, HRAs can vary widely. For example, your employer can also entirely determine the expense types that can be reimbursed through the HRA.

Although the funds are there for eligible individuals to use, an HRA doesn’t follow you if you leave your place of employment.

How to Enroll in an HRA

Just as with a group health insurance plan, your organization has an enrollment period. Some plans feature an automatic enrollment period, but you check your company’s annual enrollment documentation to learn how to enroll when the time comes. This is typically near the end of the year.

What Is a Health Savings Account (HSA)?

A Health Savings Account (HSA) is a spending account owned by the employee – as opposed to an HRA, which the employer owns. An HSA is like an HRA in that there are tax advantages with enrollment. The employee funds the account with their own money, but they are not subject to federal income tax at the time of deposit.

One caveat to enrolling in an HSA is that the employee must enroll in a Deductible Health Plan (HDHP)” data-wpil-keyword-link=”linked”>High Deductible Health Plan (HDHP). An HDHP has a minimum deductible of $1,400 for an individual and $2,800 for a family. However, these numbers can change annually.

The annual contribution limit for an HSA in 2022 is $3,650 for an individual or $7,300 for a family. An HSA is ideal for someone seeking tax relief on medical procedure costs. However, it’s important to understand the fees associated with HSAs.

How to Enroll in an HSA

There are two ways to enroll in an HSA: you can either register through your employer or as an individual. When your employer offers an HSA, you can contribute your funds directly from your paycheck. Every employer-based HSA will have its nuances, so check with them for the exact enrollment process. If you choose to set up your own HSA through a bank, they will walk you through the process, and you can contribute your funds however you see fit.

Key Differences Between HRAs and HSAs

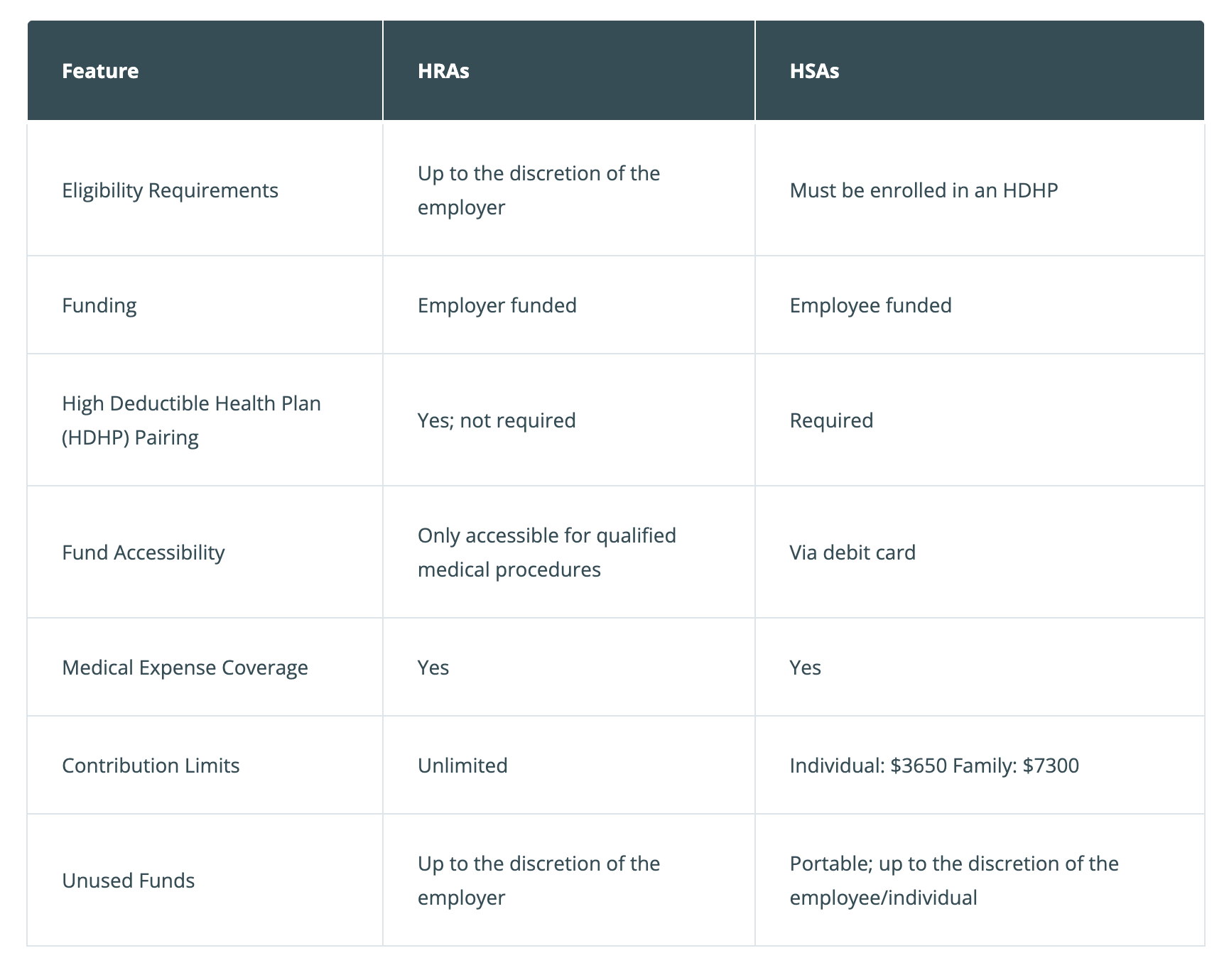

The most significant difference between an HRA and an HSA is who funds each account. Only the employer can fund the account with an HRA, and with an HSA, the employees and employers fund the account.

HRA

You’re eligible to enroll in an HRA if you are a current or former W-2 employee for a company that offers an HRA. Your qualified dependents are also eligible to participate.

HSA

You must enroll in an HDHP to be eligible for an HSA. Some HSAs are provided by employers, but you can also enroll in one independently through the Marketplace or certain banking institutions.

Funding

HRA

With an HRA, the funds are added solely by your employer, at their discretion. The employer determines eligibility and the number of funds that you can access.

HSA

With an HSA, the funds are added solely by you, the employee. The yearly limits for HSA deposits depend on whether you use self-only HDHP coverage (which has a maximum of $3,650) or are enrolled in an HDHP for your family (which has a maximum of $7,300).

High Deductible Health Plan (HDHP) Pairing

Both HRAs and HSAs can be paired with an HDHP. The function of pairing an HSA and an HRA with an HDHP is the same: to help employees pay for health coverage. However, the actual pairing process is different.

HRA

Unlike an HSA, with an HRA, you don’t need to be enrolled in an HDHP to sign up. However, many people choose to enroll in an HDHP to help offset the costs of medical services.

HSA

To enroll in an HSA, you must be enrolled in an HDHP. When you enroll in an HDHP, the health plan determines your eligibility for an HSA.

Fund Accessibility

An HRA and an HSA are both similar in that funds are added either by you or your employer. However, if you need to access these funds, the process differs between the two.

HRA

Most employers provide a debit card tied to your account to withdraw funds from an HRA. Another way to access the funds provided in an HRA is to pay the expenses upfront and request a reimbursement. With an HRA, you can only withdraw funds for medically approved procedures.

HSA

You can withdraw funds from your HSA just as you would take out funds from your bank account. However, if the cash you take out isn’t for medically approved procedures, it must be reported, and you’ll lose your tax-shielding benefits for that amount withdrawn.

Medical Expense Coverage

Medical expense coverage, commonly referred to as a Medical Expense Reimbursement Plan (MERP), typically offers an allowance of tax-free money as an option to group health insurance. MERPs can help to offset the cost of medical expenses through the following benefits:

Tax savings: Employee reimbursements are tax-exempt, and the employer’s contributions are tax-deductible business expenses.

Flexibility: One can use MERP funds for a variety of medical expenses.

Control: The employer decides how much to allocate in MERPs.

Freedom: Employees can enjoy a single point of contact.

HRA

The qualified small employer HRA (QSEHRA) is an example of a stand-alone MERP designed for employers with fewer than 50 full-time employees. This allows employees to purchase their ideal health insurance plan and know that their medical expenses are covered.

HSA

One can pair a MERP with an HSA, but you do not have to have any health coverage to participate in a MERP.

Contribution Limits

Contribution limits for an HSA and an HRA differ. There is no contributory limit for an HRA, and the limits for an HSA are capped at a specific amount for individuals and families.

HRA

An HRA is an employer-funded account, and there are no yearly limitations on how much is contributed. For most employers, the more contributed, the better, as all funds receive tax benefits.

HSA

An HSA is employee-funded, and the government regulates the amount each person can contribute. The annual contribution limit for an HSA in 2022 is $3,650 for an individual or $7,300 for a family.

Unused Funds

What if you have unused funds at the end of the year in your HSA and HRA — where does this money go?

HRA

When an employee leaves the company, unused HRA funds are usually returned to the employer. However, since only employers contribute funds to an HRA, what they do with unused funds is entirely up to their discretion.

HSA

Since an HSA is funded solely by you and not your employer, any unused funds are yours to keep. If you leave your place of employment, an HSA is portable, as it can travel with you to your new job.

Can You Have Both an HRA and HSA?

You can have an HRA and an HSA simultaneously, but only in specific circumstances. To be eligible for an HSA, you must be covered by an HDHP and not be enrolled in any other health plan. There are three main types of HRA plans compatible with an HSA:

Post-Deductible HRA

A post-deductible HRA is a specific HRA plan designed to integrate a qualified high-deductible health insurance plan (HDHP) and a health savings account (HSA).

Retirement HRA

A retirement HRA — sometimes referred to as a “retiree” HRA, or “RHRA” for short — is an employer-funded account created to assist retired employees. These HRAs help pay for plan-eligible medical expenses during retirement, including individual health insurance and Medicare premiums.

Limited-Purpose HRA

Limited-purpose HRAs allow employers to reimburse employees for dental, vision, and preventive care costs. Employers can offer this limited-purpose HRA in conjunction with an HDHP, thus allowing employees the opportunity to use HSAs to save for future medical expenses.