Understanding The Different Types of Life Insurance

Life insurance serves as a financial safety net for families, providing monetary support in the event of a family member’s death. In short, a life insurance policy provides financial protection for your loved ones and mitigates the loss of your income when you die.

Depending on the type of life insurance policy you choose, you can also use it as a cash value accumulation tool.

Various types of life insurance exist, including term life, whole life, and universal life. Each caters to different needs and financial goals. Learn more about these types of policies and how they could work for you with our guidance.

An Overview of Options: Term vs. Permanent Life Insurance

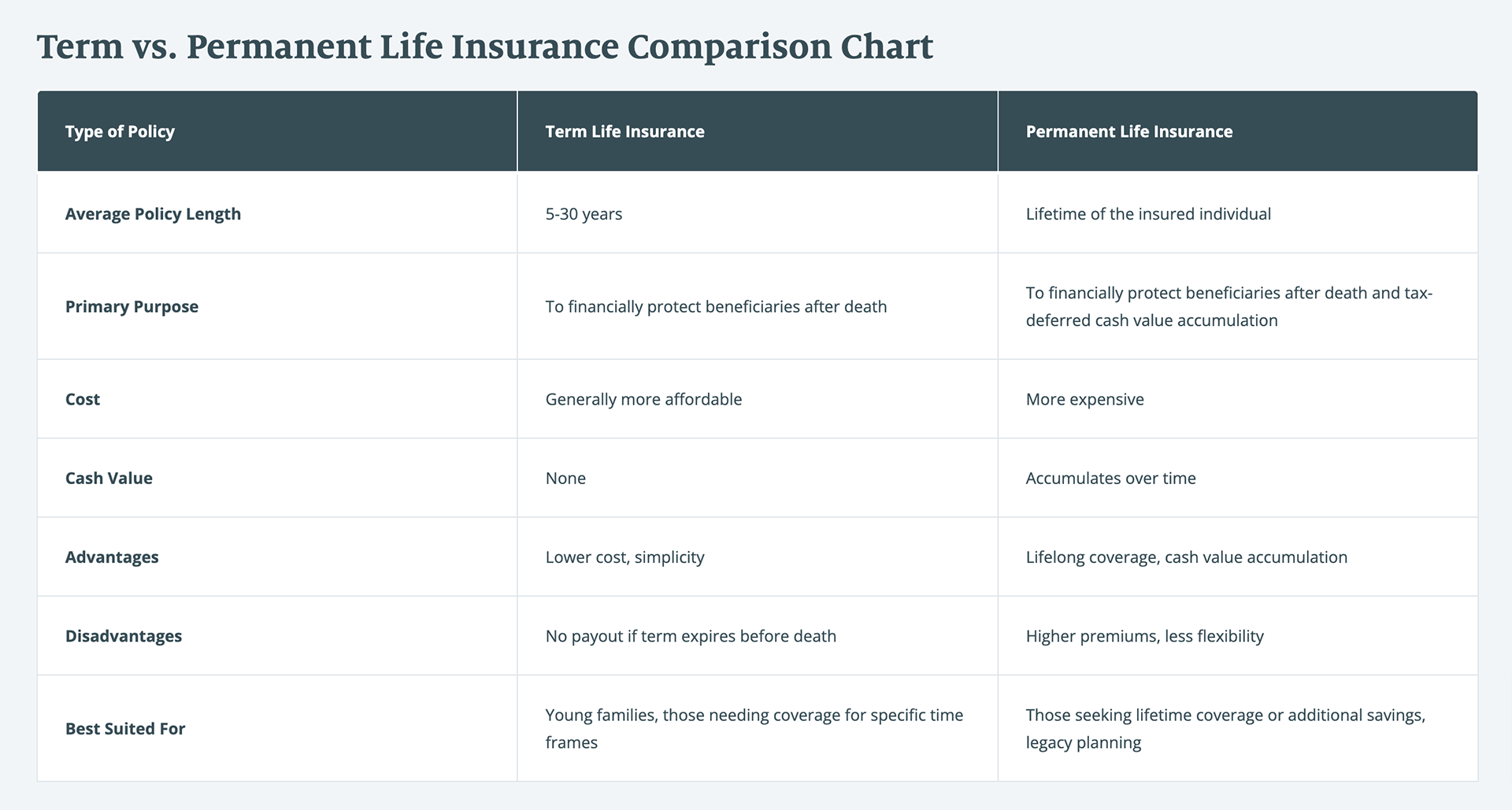

The two main types of life insurance options are term and permanent life insurance. Term life insurance policies typically only provide coverage for a set period of time, known as the policy’s term. If the insured individual passes away during that term, the insurance company pays the beneficiary the death benefit.

If the policyholder outlives the term, there is typically no payout.

Permanent life insurance, on the other hand, is active for the policyholder’s entire life as long as the premiums are paid. This means there's a guaranteed payout.

In addition, many permanent life insurance policies accrue a cash value, which can be used for estate planning, to support dependents long term, or as an income source during retirement.

Term vs. Permanent Life Insurance Comparison Chart

Understanding Term Life Insurance

Term life insurance is a policy that provides coverage for a specific period or “term,” such as 10, 20, or 30 years. It’s generally more affordable than permanent life insurance and offers a fixed death benefit. However, it has no cash value, and coverage ends if the term expires.

Term life insurance can be ideal for young families needing large coverage for a set period, like while children are dependent or a mortgage is being paid. For example, a 30-year-old parent may choose a 20-year term to cover child-rearing and educational expenses.

Term Life Insurance Types

Renewable term life insurance: A renewable term life policy allows the owner to renew at the end of its term. Although the premium price will increase, you will not have to undergo a new health evaluation, which can be important as you age.

Convertible term life insurance: A convertible policy lets the owner convert their term policy into a permanent one. You can start with a term insurance policy, then as your income increases, you can convert to a permanent policy and begin accumulating a cash value.

Group life insurance: Group life insurance is an employee benefit provided by some employers. Group term provides a fixed death benefit, a level premium, and no cash value. It is only active as long as you stay with your employer.

Supplemental life insurance: A supplemental policy is a type of term life insurance which is intended to strengthen the coverage of an existing policy. If a basic policy does not provide the coverage you need, you can add on supplemental insurance to fill in the coverage gaps. A supplemental policy that adds your spouse or child to your policy is a common supplemental add-on.

Mortgage and credit life insurance: When a borrower takes out a mortgage loan, they can get a mortgage life insurance policy or a credit life insurance policy on the loan. The policy’s monthly payment is factored into the cost of the mortgage payment. If the borrower dies before the loan is paid in full, this policy pays the remaining balance.

Understanding Permanent Life Insurance

Permanent life insurance policies provide coverage for the entire life of the policyholder as long as the premiums are paid. Most permanent policies can grow cash value, which can be used however the policyholder wishes. In addition, there are living benefits the policyholder can use for long-term care or other financial needs.

Permanent life insurance can be ideal for those seeking lifetime coverage or an additional savings mechanism, like someone wanting to ensure estate liquidity or leave a financial legacy regardless of when they pass away.

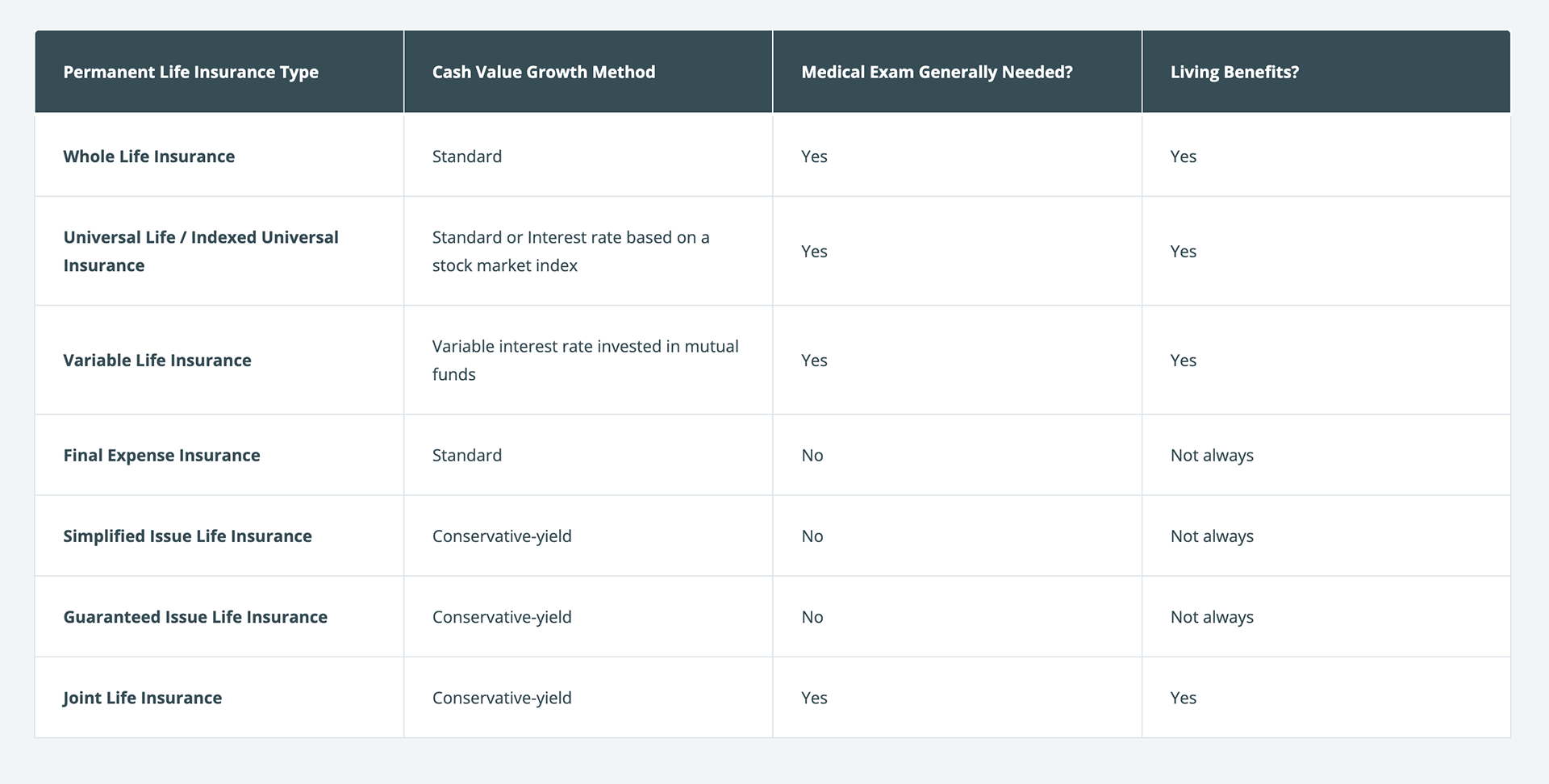

Types of Permanent Life Insurance

Whole life insurance: Whole life insurance is a type of permanent policy that builds cash value over time, and the cash value accumulates from a percentage of the premium amount as it’s paid. The premium levels are fixed, as is the death benefit, so they won’t fluctuate over the life of the policy.

Universal life insurance: Universal life insurance is similar to whole life, except the premiums and death benefit are flexible rather than fixed. Another distinction is that the cash value earned on a universal policy can fluctuate based on current market rates if the policy holder has chosen the indexed option for their refunds. This means that the interest rate earned can change.

Variable life insurance: Variable life insurance includes equity funds, money market funds, bond funds, and various stocks. Variable policies are considered securities contracts due to inherent investment risks and are regulated by federal securities laws. With a variable policy, the death benefit can be linked to the performance of the separate account funds.

Final expense life insurance: With final expense insurance, the policy’s death benefit is usually lower to only cover final expenses like burial costs. It’s commonly referred to as burial insurance or funeral insurance and is designed for older adults who are making end-of-life plans.

Joint life insurance: Joint life insurance is a type of policy designed for two people, such as spouses or domestic partners. Depending on the specifics of the policy, benefits can be paid out when one or both policyholders die.

These types of life insurance policies can also be offered as term insurance, but the majority are offered as permanent insurance policies regardless of when they pass away.

Different Types of Life Insurance by Underwriting

Life insurance underwriting is a process your insurer undertakes to determine your eligibility and rates. A life insurance underwriter assesses your application questionnaire answers, lifestyle, and medical exam results to calculate your mortality risk. Typically, the more risky you are deemed, the higher your premium may be.

Some life insurance companies can decline coverage if you are deemed to be too high risk of an applicant. For this reason, there are several different types of life insurance based on how they utilize underwriting during the application process.

Fully underwritten life insurance: This type of policy involves a comprehensive evaluation process, including medical examinations, health history, lifestyle assessments, and sometimes even financial review.

There are potential cost savings for healthier individuals because of the more accurate pricing based on detailed information.

Simplified issue life insurance: For those concerned that their health may limit their ability to get permanent life insurance, a simplified issue policy is an option. With this type of policy, there are minimal health questions and no medical exam requirement. This is ideal for those looking for coverage quickly.

Guaranteed issue life insurance: With a guaranteed issue life insurance policy, there is a guaranteed death benefit. This type of permanent policy is available without a medical exam, so it’s geared toward those who are not eligible for other types of life insurance policies. Coverage amounts are typically lower.

Life Insurance Riders: Enhancing Your Policy

A life insurance rider is an additional provision added to the main policy, allowing customization of coverage. These can be added at an extra cost, often at the policy’s inception, to enhance or modify standard coverage.

Common Life Insurance Riders

Accidental Death and Dismemberment (AD&D): Accidental Death and Dismemberment (AD&D) life insurance specifically covers accidental death or serious injury leading to dismemberment. With this rider, if the policyholder suffers a fatal accident or loss of limbs, sight, or hearing, the death benefit could double. Exclusions might include deaths from non-accidental causes, drug overdoses, or specific high-risk activities.

Waiver of Premium: A Waiver of Premium rider exempts the policyholder from paying future premiums if they become disabled or critically ill and are unable to work due to a covered event. The insurance company waives the premium payments while keeping the coverage active, ensuring that the policy remains in force even during times of financial hardship due to health issues.

Child Rider: A Child Rider offers a death benefit that can help alleviate the costs associated with funeral expenses or other unexpected expenses associated with a child’s death. It is a way for parents to extend some level of insurance protection to their children within their own life insurance policy.

Choosing the Right Life Insurance

Assess your needs. Consider financial situation (income, debts, assets), age, health, and family needs.

For example, if you are younger and do not have dependents, a term life insurance policy can provide cost-effective protection to plan for the future and cover debts.

But retirees may want to consider final expense or universal life insurance options instead to focus on legacy planning and funeral costs.

Determine the amount. Use the 10X salary, DIME method, or work with a professional to calculate how much life insurance coverage you need to accomplish your goals. For example, if you are trying to cover a large debt, you may need to factor in how much that debt will grow or shrink over time.

Compare insurance companies. Utilize online comparison sites or consult with insurance brokers and agents to compare policies, premiums, and company reputations.

Choose and apply. Select the best-fitting policy and complete the application, potentially undergoing a medical exam if required. Keep in mind that continual review and adjustment of your policy are vital as life circumstances change.

Putting It All Together

Each type of life insurance, such as term life, whole life, universal life, and variable life, offers unique features and benefits.

By understanding these differences, you can select a policy that best suits your budget, coverage requirements, and long-term objectives, ensuring that you’re investing in a policy that provides the right level of protection and financial security for you and your loved ones.

For example, term life insurance is often a better choice in scenarios where temporary coverage is needed for a specific period, such as if your budget is tight.

This is because a term policy can offer substantial coverage at an affordable cost, allowing you to prioritize immediate protection.

However, permanent life insurance is a better choice in situations where lifelong coverage and potential cash value accumulation are important, such as if you want to ensure there’s a guaranteed payout to cover your final expenses, such as funeral costs and outstanding medical bills.